Recent Inflation Thoughts

Recent Inflation Thoughts

Consolidating some recent ideas on inflation

Basic Ideas

This note consolidates some of my recent analysis related to inflation and the prospects for reduction. The basic concept is that the small open Canadian economy has evolved significantly from the 70s and may not respond to the simple nostrums of that period. Import penetration provided lower prices and more competition in the supply sector. This provided gains on the inflation front. However, limited competition has provided scope for the distribution sector to expand their margins at the expense of consumers, particularly in the price-inelastic food sector.

The Context

Two charts will be used to show the context for my thinking. Click on the charts as needed to enlarge.

The important point is that food, energy, and shelter costs are key issues in the inflation perspective of most of us. Food costs have risen and are still rising due to harvest/weather issues as well as war-induced price rises for key input and output commodities in the farm sector. Energy prices are largely determined in world markets.

Service prices are a big element of the CPI. The right-hand chart shows the most important components of the CPI services aggregate by weight. Recent monetary policy moves have escalated mortgage costs with a direct effect on housing purchase costs and rent. Mortgage rates feed into rents directly through demand shifts and indirectly through costs as landlords try to recoup their increased mortgage expenses. Interest rates are the direct purview of the Bank of Canada.

Energy costs are critical and are largely exogenous to Canadian public policy. Higher interest rates will make it more expensive to bring more energy-efficient physical capital into play and will not lower world prices.

Purely domestic wages play a much smaller part than might be conceived from the aggregate Services title. Many service prices such as public and private transportation are dominated by external energy costs or external suppliers in the case of air transport. Restaurant and take-out meals are dominated by food costs. Insurance prices are not driven by broad wage costs but rather by other factors such as climate change and the costs of repairing high-tech vehicles. Property taxes are a policy item that is not likely to be reduced by higher interest rates. Raising interest rates is unlikely to lower the price of financial services.

Imports are Critical

Compared to the 1970s, Canada is even more exposed to foreign price shocks which are not really influenced by Canadian demand reduction. We are a small open economy. Import intensity has increased dramatically. The next chart compares the movements in the aggregate inflation rate with the relative intensity of imports in the economy. The latter is depicted using the ratio of import ($K) volume to population from the national accounts.

The essential message is that imports are 6 times as important now as in the 1970s to the domestic economy. They are particularly critical for consumer expenditure. Free trade and globalization have given Canadians access to a global marketplace with lower prices and more competition on the supply side. This has provided much of the inflation reduction and radically lowered the importance of domestic supply for the economy, particularly the consumer sector. However, foreign supply shocks feed directly into consumer prices.

This point is further emphasized by some charts from my annual consumption analysis. We import most of our consumer durables and semi-durables. Our non-durable food and energy consumption are also strongly influenced by world prices.

The orange bars show the import share in the final consumer price. The green bars show the trade (distribution) margins. The dark bar is the indirect tax portion. The pink bar is the portion of the price accounted for by domestic production. The services portion has a high domestic content because of the housing element, particularly the expense associated with implicit rental income from owning your own home.

The most volatile durable and non-durable prices have been dominated by imports. Domestic monetary policy can affect prices only in so far as distribution margins respond to demand. The prices of price-inelastic commodities such as food and energy do not respond well to attempts to reduce demand through higher interest rates. We all need to eat and heat our homes and our merchants know that. They know that they can not make up in volume what they lose in revenue through price reductions.

We have benefited from import penetration because of the impact on prices. Imports were cheaper. However, the domestic influences on prices have become more restricted.

Producer Margins are an Issue

It is my contention that the inflation rhetoric of the talking heads provided room for the domestic sectors to expand their margins. This has been particularly true in sectors with less competition such as food and gasoline retailing. The chart below displays service margins. These are simply an index of the difference between the price paid for goods and the price received. Thus, all operating costs are incorporated as well.

The rapid rise in margins for gasoline stations shows their ability to exploit the low price elasticity of their product. Food is essentially price inelastic. Grocery store margins really broke upward with the start of the pandemic. Margins for specialty stores rose faster than for supermarkets. With low price elasticities, merchants have more discretion to mark up cost increases. The general merchandise sector also benefited from their ability to compete in the food space with grocery stores.

The highly competitive clothing sector is the only major category showing declining margins. Price elasticities are high for women’s clothing in particular and relatively low for men’s wear. Hence, the rising margins for men’s clothing seen in the next chart. Men may not be as price-conscious shoppers.

The myriad banner stores carrying the same brands of shoes is possibly the factor behind the declining margins in that sector.

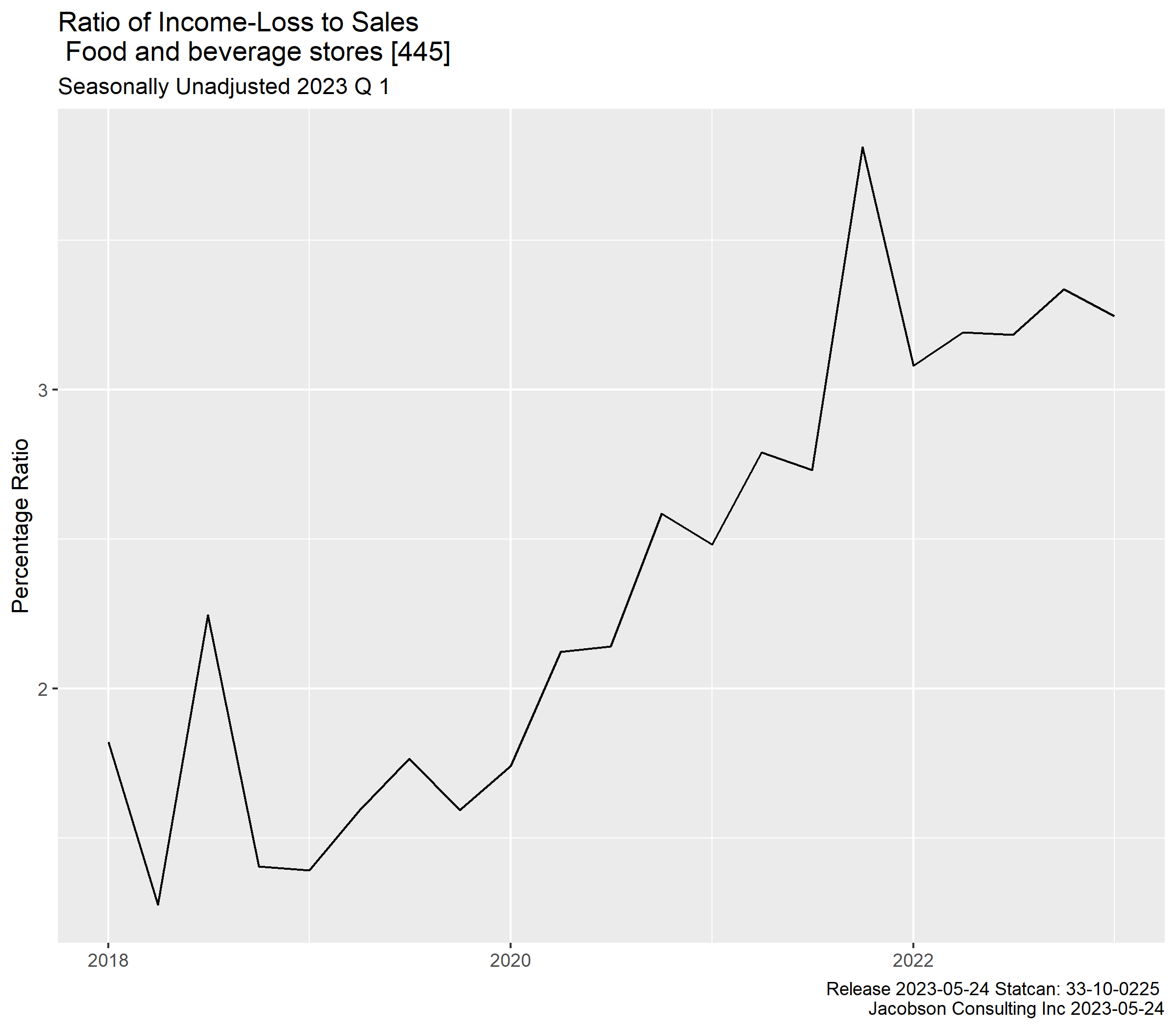

The next charts display a form of profit (net of expenses) measure. The charts show the ratio of sectoral/aggregate net income, denoted as income-loss, to sales.

In the competitive clothing and general merchandise sector, the income ratio has settled back to a stable rate similar to the pre-pandemic period.

However, in the last competitive grocery sector, the income-sales ratio has moved to a much higher plateau in the post-pandemic period.

These gains in the income rate have occurred despite the volume losses to the general merchandising sector. In short, grocery merchants are exploiting the less competitive market place to raise their returns above the pre-pandemic norm.

My GDP charts shows food retailing (orange) is on a downward trend relative to other retail sectors.

Dairy Prices

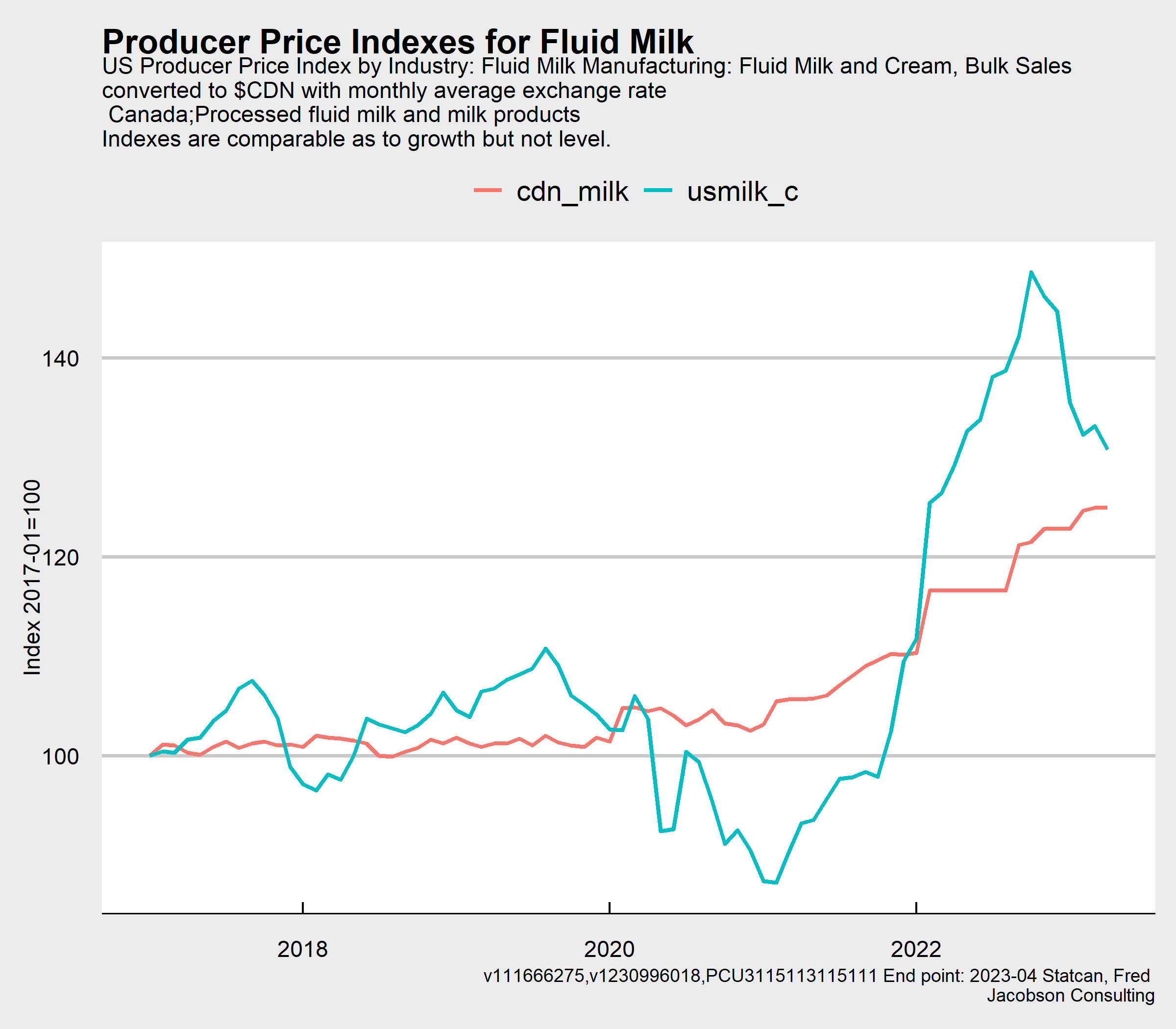

There has been a lot of rhetoric not matching reality about dairy prices in Canada. Earlier posts have discussed the fluid milk marketing regimes in Canada and the US. There are quality gains in the Canadian system with respect to the block on using hormones to drive production about the levels possibly appropriate for the animals. More importantly, stable returns provide a stable milk supply. The first chart compares the producer price for fluid milk in Canada and the US.

'The more volatile US price led to extreme volatility in the US retail market.

The real issue is the management of dairy prices in Canada. The price paid to farmers for raw milk is managed but retail prices are left to the processing and distribution sectors. Because it has recently been in the press, the next chart shows the relationship between the raw milk price received by the farmer and the retail butter prices faced by the consumer. Because there are regional differences, Ontario prices are used.

The CPI price has been used because this is a '“constant quality” measure. The raw milk price actually dropped prior to the pandemic and then was raised to reflect higher feed and other production costs (including interest). A LOESS trend has been overlaid on top of the seasonally-unadjusted prices to highlight the movement. The essential message is that the production and distribution sectors have expanded their margins before and after the pandemic shutdown.

Summary

The summary messages are:

Imports now play a strong role in determining the prices paid by consumers.

The competitive nature of domestic markets may strongly influence inflation outcomes in the short run. With less competition, firms can more easily pass through and mark up cost increases.

The Services grouping in the CPI is a bit of a misnomer. Persistently high levels of service price inflation primarily reflect supply constraints in residential construction, rising mortgage interest rates and higher travel-related energy costs, rather than increasing wage costs.

Key elements of the CPI represent price-inelastic goods and services such as food, energy and shelter. These may not respond as expected by some analysts to interest rate increases.

The rise in Canadian inflation was largely driven by global forces and exacerbated by the lack of supply competition in certain sectors.