Food Price Inflation

Food Price Inflation

A consolidation of ideas with charts. Enlarged chart versions are available using the web link.

Outline

#food #inflation #canada - Food price inflation seems to be top of mind in most households. Certainly, in ours, it gets more focus than the broad CPI which has too much influence from factors such as airline travel or car prices which are not not directly relevant to many households every month. This note will discuss supply factors, including imports, agricultural cost factors and retail competition. My contention is that these factors cannot be effectively managed by manipulating broad credit conditions.

Food Demand

Domestic food consumption is largely considered to be a necessity for most people. Generally, more affluent households will spend more on food, both because of taste and the size of household. Food is broadly considered to be inelastic with respect to price. In other words, consumption will decline less than proportionately to the rate of price increase. A 2007 study prepared for Agriculture Canada provides statistical support to this point.

Ruth, Pomboza, and Mbaga Msafiri. "The estimation of food demand elasticities in Canada." (2007).

Food inflation has remained relatively strong but is declining.

Prices vary over time and region

The next charts show variations over time and region for selected products. The prices are derived by Statistics Canada from scanner data.

The main points are that the price change is not uniform by province and that the average levels, by region, are different for the selected products.

This suggests that there are regional competition, distribution and supply issues.

Sources of Supply

In commodity terms, imports make up a significant share of fruits and vegetables. However, domestic supply is significant. These charts show trade as a share of the disposition of the product in the Canadian market. Canada is now exporting peppers. The import share of lettuce has declined.

We produce a lot of what we consume but food is also an export industry for us. For example, imports were once the only supply for sweet potatoes. Now, we export almost half of the total available.

Meat trade has also become significant. We have the capacity to export but we also import. Pork exports have become particularly significant. We import a significant share of our lamb usage and also industrial (stewing) hens.

The important point is that we are exposed to foreign prices over which we have no policy control. With open markets, our domestic supply will also be priced in world terms.

Farm Input Costs

Statistics Canada produces a wealth of agricultural data. Fertilizer and grain crop prices skyrocketed in early 2022 with the invasion of the Ukraine by Russia. Harvest issues in many parts of the world did not help the problem. Broadly, the rate of increase has stabilized and is now declining. The limited competition in agricultural input supply and marketing may also be a factor.

Machinery fuel prices (general chart) spiked but have roughly stabilized at the new higher level. The essential point is cost increases may be stabilizing. These external factors are not related to the availability of credit. However, interest costs are a business expense in farming as in other sectors.

The declining input costs may help to reduce the prices that farmers receive for managed products. However, commodity prices that are set at the world level will require market stability to decline. Good harvests to increase supply will help.

Dairy Prices

Many commentators consider dairy to be an issue because of Canadian supply management. The chart on the left compares the producer price for fluid milk in Canada and the US. The US volatility and growth are startling in comparison to Canada suggesting that our supply management policies may be providing stability to the farm market but not excessive price growth.

The chart on the right shows the retail price of butter in Ontario relative to the raw milk price. The obvious point is that the product price grew much faster than the revenue to farmers. Issues in the post-farm system need to be considered.

It is also important to note that the raw milk price (right hand chart) declined as well as rose but the retail price did not. The Canadian producer producer price (after processing -red line) shown in the left-hand chart did not.

The retail price clearly grew much faster than the price received by farmers. Post-farm margins increased raising the impact of rising farm prices on consumers.

Food Distribution

The grocery sector is dominated by a few major retailers. There is significant indications that the level of competition is inadequate, particularly at the local level.

In comparison to general merchandisers, the ratio of net income to sales expanded significantly during the pandemic. This may be a reflection of the trumpeting of “back to the 70’s” inflationistas which may have made consumers more tolerant of price increases.

The profit rate in the grocery segment is very low and clearly shifted up during the pandemic. This is establishment data which will not reflect any consolidation of non-grocery units such as health and beauty. There is no indication of an acceleration in labour costs. The annual charts (above) show that labour costs did not spike relative to the costs of goods sold during the pandemic for grocers but the profit rate rose.

Statistics Canada also reports service prices which are an index of the difference between what is received for goods sold and what is paid. The service price for grocery stores has risen significantly during the pandemic

Food stores are shown in contrast to the much more competitive clothing sector. The service price for the latter has declined.

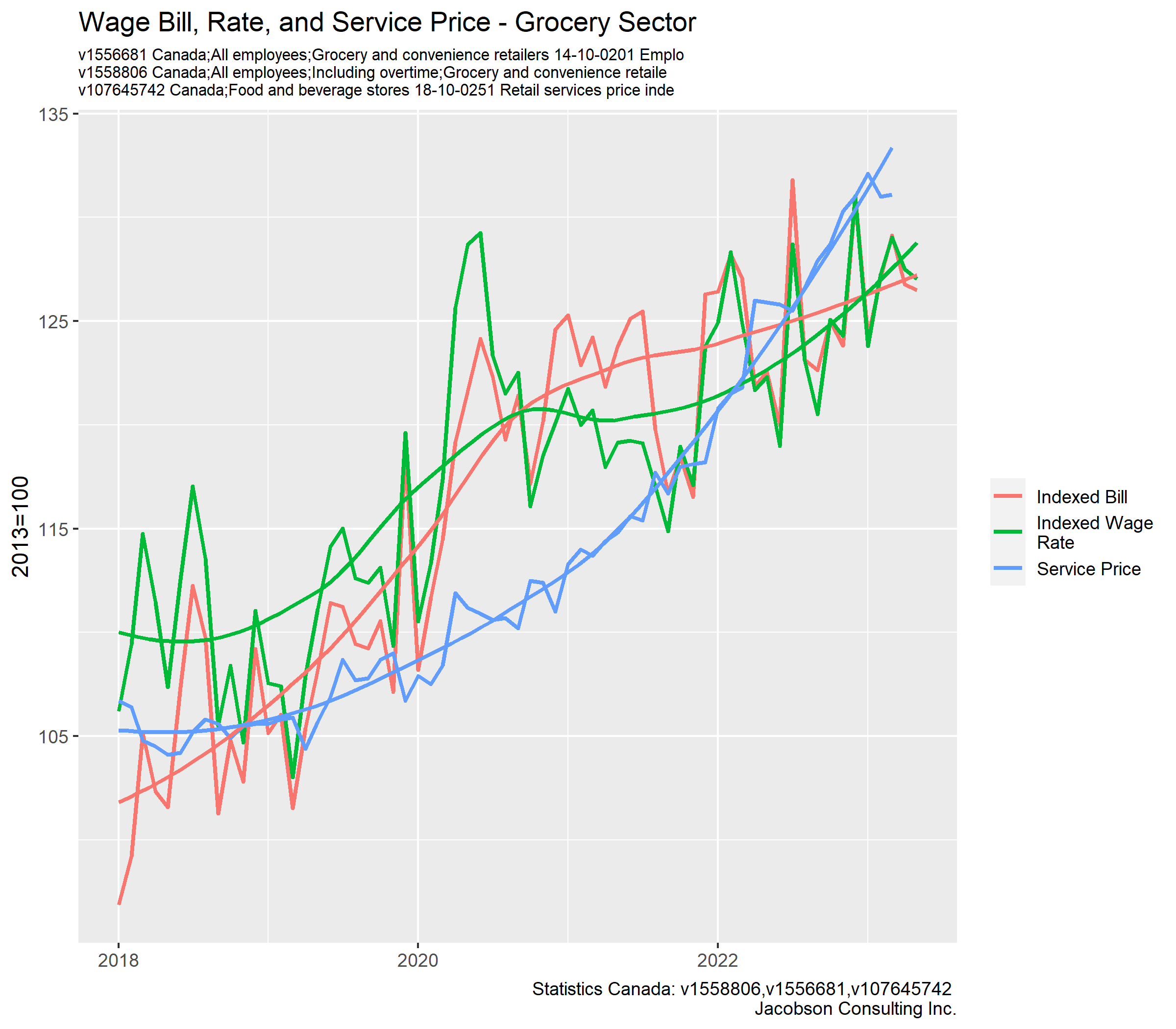

As a confirmation that labour costs are not the driver, the next chart compares an index of the wage rate and bill to the service price index. The average wage rate rose with the pandemic adjustments in early part of 2020 when low-wage workers were not required. Recently, the service price, which includes all non-goods costs, is clearly growing much faster labour costs.

The increased margins of the grocery sector have not driven food inflation but they have added insult to injury for consumers.

Policy Issues and Summary

There are many issues with the efficacy of monetary tightness to control broad inflation. Many policy heresies have been under discussion. Professor Rodrik provides a nice summary which merits review.

Rodrik, Dani. "Inflation Heresies." Project Syndicate (2022).

This note has tried to show the complexities of the factors affecting the food prices faced by consumers. The bottom line is that these factors are largely beyond the scope of monetary demand management. Labour costs cannot be used as an excuse for the problem. Marketing boards (dairy, eggs) provide stability but are not the source of the problem.

The supply cost factors will resolved with market stability and increased supply. We need to look at other policies to manage the aggressive margin increases in the post-farm sectors. Price controls are considered by some to be too radical and difficult to implement. The high quality price data now available from scanners might make regulation more feasible.

Calls for tougher competition policy are coming a little late after all the mergers. It would be a challenge for government to effectively encourage entry into markets that are dominated by a few retailers with substantial command of locations and logistics. There is policy work to be done.